10-14/2022

Monthly Evaluation of Melamine: The Market Rose First And Then Fell (September 2022)

Date : October. 10 2022|Announcer : admin

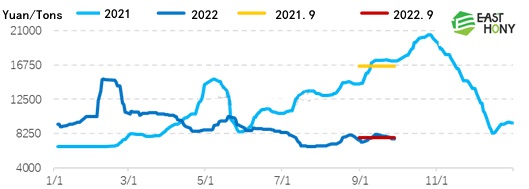

1.Market review of this month

Analysis of domestic melamine price trend

Figure 1

At the beginning of this month, due to the maintenance plan of some enterprises, it is expected that the start-up stock will decline, and the downstream market will enter the traditional consumption peak season of “Jinjiu”, there is also a possibility of increasing demand. With the continuous rise of the raw material urea price, cost support will be provided, and the industry insiders have strong bullish intentions, and the price will gradually rise at the beginning; In the middle of the year, the new units were stopped for maintenance, and the operating load rate of the enterprise dropped to about 50%. In addition, the local logistics transportation was not smooth, which led to the slow circulation of goods in some markets, tight supply, and further increase in prices. However, due to the slow start up of the downstream factories as a whole, insufficient demand follow-up, and various levels of early inventory, downstream fear of heights is growing, sales pressure is emerging, and deals tend to be loose. In addition, close to the National Day holiday, some manufacturers actively received orders, so the space for negotiation was further expanded, which lowered the overall transaction focus, and the price continued to decline to the end of the month in the last ten days.

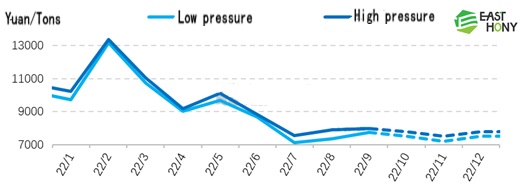

2.Market analysis and forecast of next month

Figure 2

From the perspective of cost, the raw material urea market will fluctuate at a relatively high level and narrow range in the later period, which will also provide cost support for melamine to a certain extent.

In terms of supply, some of the equipment stopped production in the later period will resume production in succession. Although it is still possible to store and park the equipment, the overall starting load level of the enterprise may be increased to more than 60%, the output will increase, and the supply of goods will be relatively abundant.

From the perspective of demand, October is still in the traditional consumption peak season. Downstream factories continue to orderly produce according to orders. Rigid demand still exists. In addition, exports are relatively stable. However, due to the fact that there will be different levels of inventory in the early downstream procurement, bargain hunting is the main way to follow up.

In addition, for the forecast of the next three months, it is expected that the overall fluctuation space of the market in the fourth quarter is also relatively limited, the supply is abundant but the demand is difficult to improve significantly, and the supply and demand pattern continues to be loose.